7 challenges with blockchain adoption and how to avoid them

Organizations tend to face the same hurdles when they try to implement blockchain. Knowing what they are could be the first big step to overcoming them on the road to success.

Blockchain technology is often surrounded by plenty of hype, which makes many business leaders keenly interested in adopting it but also concerned about blockchain challenges and risks.

At its most basic, blockchain refers to peer-to-peer distributed ledger technology that can record transactions between two parties efficiently and in a verifiable and permanent way, enabling tracking and traceability. This emerging technology has game-changing potential for a wide range of applications that go far beyond its roots in cryptocurrency.

Consider the following examples:

- Pharmaceutical companies have developed blockchain applications to secure supply chains for medicine and confidential test data.

- In collaboration with IBM, Walmart developed a blockchain system that cut product tracing times from seven days to 2.2 seconds.

- Microsoft has secured about 40 patents for blockchain-based payment gateways and secure storage.

Along with the benefits that some early-adopter organizations are getting from blockchain, broader awareness of the technology is growing at a rapid pace. Data from a 2020 APQC survey of supply chain professionals showed that 66% of organizations were familiar with blockchain in 2019 -- a number that grew to 80% within a year. That said, the majority of organizations were still in the early stages of adoption.

Why did only 12% of participants report that they were live with either blockchain or blockchain as a service? What was holding back the 34% of respondents who were not even exploring the use of blockchain?

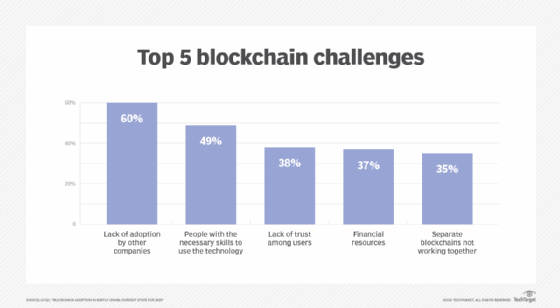

The top five blockchain challenges organizations faced, according to the APQC survey, were lack of adoption, skills gaps, trust among users, financial resources and blockchain interoperability.

While newer Gartner research from 2023 indicated that many blockchain challenges have yet to change, it also alluded to two other common themes: the speed at which blockchain products reach the market, and lack of regulatory clarity.

Read on to explore why these blockchain challenges persist, along with ideas on how to address them.

1. Lack of adoption

Blockchains are ecosystems that require broad adoption to work effectively. For example, track-and-trace capabilities in supply chains not only require an organization to adopt a blockchain network but for its suppliers to do so as well. APQC found that only 29% of organizations were piloting blockchain or had fully deployed it.

At the time, there was hope that adoption of blockchain would grow. Organizations were coming together and forming collaborative blockchain working groups to address common pain points and develop solutions that could benefit everyone without revealing proprietary information.

Research from Gartner, however, indicated that these challenges persist in 2023. In the research firm's 2023 "CIO and Technology Executive Survey," 8% of respondents said they have deployed blockchain, a figure that is expected to increase to 46% by 2025. Despite the expected growth, numerous business, technical and organizational barriers remain.

The business issues mainly relate to customer education and hesitation. Blockchain vendors face their own issues, including partner hesitation, lack of network effect, limited skills and financial issues. Among the technical challenges are performance and limited interoperability with the necessary systems.

Gartner offered some solutions, however, and said prioritizing education and marketing initiatives are essential steps for product leaders. Showing practical uses of blockchain is also critical to winning over skeptics.

2. Skills gap

Blockchain is still very much an emerging technology, and the skills needed to develop and use it are in short supply. As the figure shows, 49% of respondents to the 2020 survey named the skills gap as a top challenge. The marketplace for blockchain skills is highly competitive and has been for some time. The expense and difficulty of talent acquisition in this area only adds to the concerns that organizations have about adopting blockchain and integrating it with legacy systems.

Gartner's 2023 data indicated that limited tech experience remains a challenge. Vendors often cite this as an issue in product development. This leads to problems creating user-friendly interfaces and adding blockchain applications to existing systems.

However, one way to counteract the skills gap is to use blockchain as a service (BaaS). Such services enable organizations to reap the benefits of blockchain without having to invest significantly in the technical talent behind it. IBM, Amazon Web Services and Oracle are just a few of the many BaaS providers.

This model has already narrowed the skills gap in the context of other technologies, such as robotic process automation (RPA). Rather than having to develop bots and write code in-house, organizations can now look to numerous vendors who have the expertise to implement RPA and customize it for each organization's needs. Users only need to know the basics of the technology and don't need to be programmers to take advantage of its benefits. Similarly, users will need to understand how to execute smart contracts, which use blockchain to automatically execute certain actions once the terms of the contract are met, but they won't need specialized knowledge about the intricacies of distributed ledgers. BaaS has the potential to mitigate the blockchain skills barrier.

3. Trust among users

Lack of trust among blockchain users is the third major obstacle to widespread implementation. This challenge cuts in two directions: Organizations might not trust the security of the technology itself, and they might not trust other parties on a blockchain network.

In theory, every transaction in a blockchain is considered to be secure, private and verified. This is true even though there is no central authority present to validate and verify the transactions, as the network is decentralized. A core part of any blockchain network is the consensus algorithms that drive common agreement about the present state of the distributed ledger for the entire network. It is meant to ensure that every new block added is the one and only version of the truth agreed upon by all the nodes in the blockchain. If it's a public -- as opposed to private -- blockchain, anyone can participate. Despite all of the mechanisms meant to guarantee trust on public blockchains, business leaders have placed greater trust in private blockchains where there are no unknown users.

Gartner research has shown that a lack of standards is also an issue. The novelty of this technology is a large reason for this problem.

4. Financial resources

The fourth barrier to widespread adoption of blockchain, according to APQC's research, is the lack of financial resources. Implementing blockchain is not free, and for many organizations the pandemic and disruption of 2020 left budgets tight. However, one other lesson learned from the pandemic is that organizations, and IT departments in particular, can change faster than previously thought possible.

A closer examination of this barrier shows that it is connected to an underlying lack of organizational awareness and understanding of blockchain. APQC has found that as awareness of new technologies becomes more widespread, the ability to effectively make a business case for their adoption improves accordingly. This will be true of blockchain as well, provided that blockchain advocates focus on building a business case that demonstrates how the benefits of the technology will offset the resources needed for implementation.

Vendors also face financial challenges in financing blockchain applications and the runtime infrastructure needed to support them, along with the inherent complexities.

5. Blockchain interoperability

As more organizations begin adopting blockchain, many tend to develop their own systems with varying characteristics -- governance rules, blockchain technology versions, consensus models, etc. These separate blockchains do not work together, and there is no universal standard to enable different networks to communicate with each other.

Blockchain interoperability includes the ability to share, see and access information across different blockchain networks without the need for an intermediary or central authority. The lack of interoperability can make mass adoption an almost impossible task.

With the impacts of the pandemic, in a business environment where collaboration across functions and with suppliers and customers is more important than ever, blockchain interoperability will be critical. It is the only way organizations will truly get the most value out of their blockchain investments. Since 2019, researchers reported seeing an increasing number of interoperability projects meant to bridge the gap between different blockchains. Many of them are aimed at connecting private networks to each other or to public blockchains. These systems will ultimately be more useful to business leaders than prior approaches that focused on public blockchains and cryptocurrency-related tools.

However, as of 2023, interoperability remains a major roadblock to the widespread application of blockchain-based tools. In fact, Gartner named interoperability as a top technical challenge, particularly with legacy systems.

Gartner noted encouraging steps to enhance interoperability across networks, including development of cross-chain communication protocols and standardized data formats.

Along with the five issues that emerged from the APQC survey, the Gartner report noted two other common challenges associated with blockchain technology.

6. Slow development pace

Blockchain technology is complicated. New products often require extensive research, development and validation. For this reason, products can be slow to come to market.

Complementary and postproduction vendors, however, do not face these issues as often. Gartner researchers surmised this is because the tools they use are more advanced.

7. Lack of regulation

According to Gartner, some blockchain vendors have indicated issues because of limited regulations during certain parts of the process. Regardless, lack of clarity about the regulatory requirements creates significant risk for blockchain providers and consumers.

Looking forward

It would be naive to claim that these blockchain challenges aren't significant barriers to its adoption. Broadly speaking, though, many of blockchain's biggest challenges are just the growing pains that are common with any new technology. In making the business case for adoption, blockchain advocates will need to convince their organizations to take the kinds of risks, form the kinds of relationships and make the kinds of tradeoffs that are common in other areas of business.

Leaders can also take steps to ensure that their products are developed in the most efficient way possible. These include publishing case studies to highlight the advantages of blockchain and forming strategic partnerships to navigate the blockchain ecosystem.

Given the benefits that organizations are already deriving from blockchain and the increasing calls for visibility and transparency between organizations, blockchain could someday be a powerful solution to some longstanding problems.

Marisa Brown is senior principal research lead at APQC, a nonprofit that offers expertise in benchmarking, best practices, process and performance improvement, and knowledge management.